Many people assume credit limits increase automatically over time. They don’t – at least not optimally. In 2026, banks increase credit card limits based on data, behaviour, and risk scoring. If you understand what they track, you can influence the outcome.

A low credit card limit can quietly restrict your financial flexibility. It affects:

- Large purchases

- Travel bookings

- Insurance payments

- Emergency spending

- Credit score utilisation

Why Your Credit Card Limit Matters

Your credit limit impacts more than spending power.

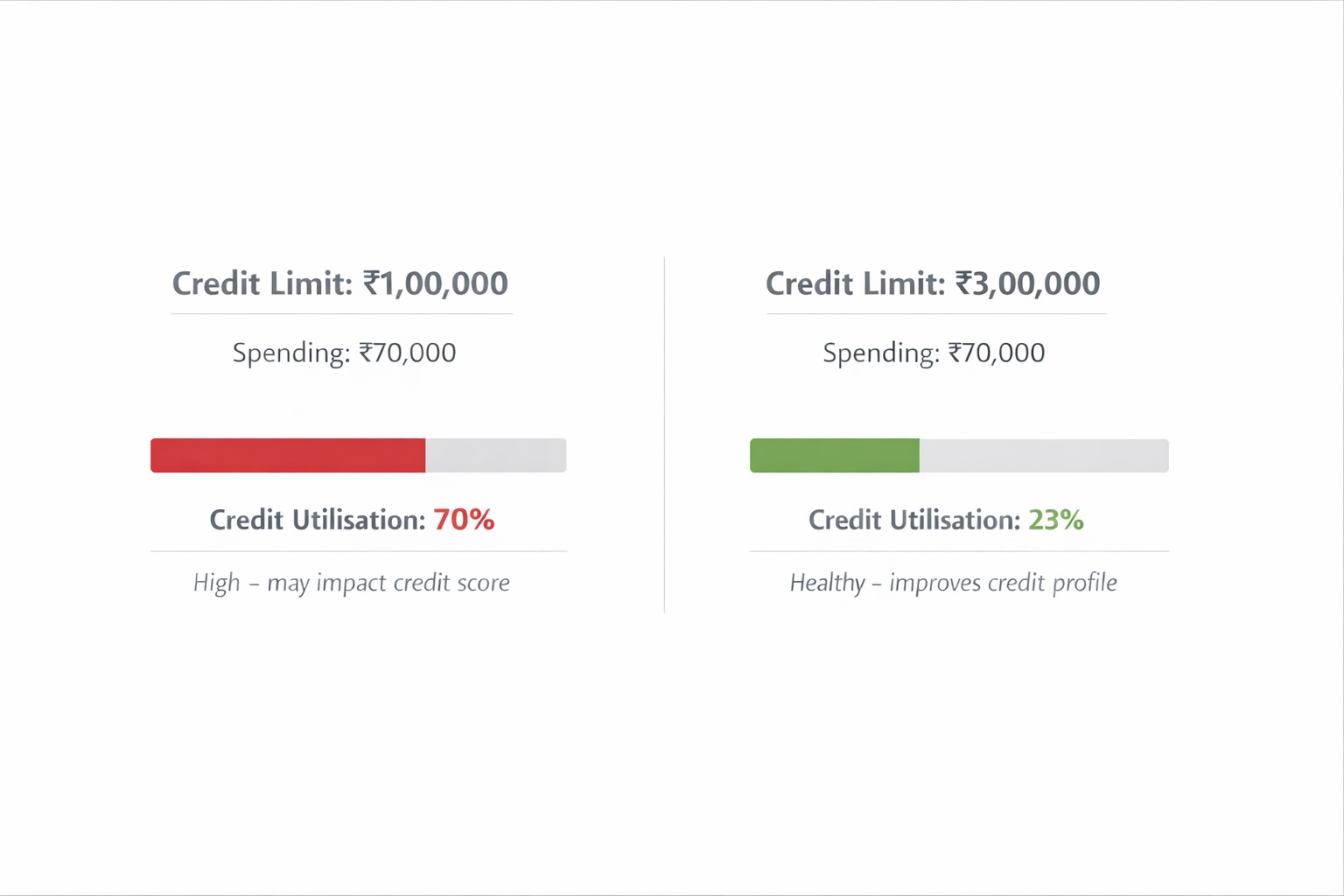

It directly affects your credit utilisation ratio, which is a major factor in credit score calculations.

For example:

If your card limit is ₹1,00,000 and you use ₹70,000, your utilisation is 70%.

That can negatively affect your credit score.

If your limit increases to ₹3,00,000 and you still use ₹70,000, your utilisation drops to 23%.

Same spending. Better profile. A higher limit improves financial optics.

How Banks Decide Credit Limit Increases

Banks evaluate multiple factors before offering an increase:

- Repayment History

Consistent on-time payments are the strongest signal of creditworthiness. - Credit Utilisation Behaviour

Using 30-40% of your limit regularly is healthier than maxing out. - Income Updates

If your salary increases and you don’t inform the bank, they don’t know. - Credit Score (CIBIL)

A score above 750 significantly improves chances. - Spending Patterns

Banks prefer customers who actively use their card.

Automatic vs Requested Limit Increase

There are two ways your limit increases:

Automatic

Banks periodically review accounts and offer upgrades via:

- SMS

- App notification

These are usually pre-approved and instant.

Manual Request

You can request a higher limit through:

- Net banking

- Customer care

- Branch visit

Banks may ask for:

- Salary slips

- ITR documents

- Updated employment proof

Manual requests are common if:

- Your income has increased

- You need a limit boost for specific reasons

When Should You Ask for a Credit Limit Increase?

You should consider requesting a limit increase if:

- Your income has grown significantly

- You regularly use over 50% of your limit

- You plan large expenses (travel, rent, insurance)

- You want to improve your credit utilisation ratio

Avoid requesting if:

- You’ve missed recent payments

- Your credit score is unstable

How to Increase Your Chances of Approval

Here’s what actually works.

1️⃣ Maintain 100% On-Time Payments

Even one delay weakens your profile.

2️⃣ Keep Utilisation Below 40%

If you consistently max out your card, banks see higher risk.

3️⃣ Update Income Information

Submit updated salary slips or ITR when income grows.

4️⃣ Use the Card Actively

Dormant cards rarely get upgrades.

5️⃣ Improve Your Credit Score

Pay all loans and EMIs on time across accounts.

Does Requesting a Limit Increase Affect Your Credit Score?

If the bank performs a hard inquiry, your score may temporarily dip by a few points.

However, once the limit increases and your utilisation drops, your score may improve.

In most cases, the long-term effect is positive.

Should You Increase Limit or Get Another Card?

Sometimes opening a second card makes more sense. Increase limit if:

- You want better utilisation ratio

- You prefer managing one card

- You’re satisfied with current rewards

Get another card if:

- You want different reward categories

- You want zero forex benefits

- You want travel perks

How Gig Income Can Support Limit Growth

Banks evaluate repayment capacity. If you earn additional income through structured gigs and can document it (via ITR), it strengthens your case for higher limits. Additional declared income increases creditworthiness. This is where layered income becomes powerful. A higher credit limit is not about spending more. It’s about:

- Improving credit health

- Increasing flexibility

- Preparing for large expenses

- Strengthening financial credibility

Credit limit growth should be intentional, not accidental.

Gig-Work Earning Opportunities with PickMyWork

Perfect for: gig workers, students, part-time earners, and anyone in Tier 2/3 cities.

How it Works

- Download the PickMyWork app

- Sign-Up with Mobile Number (no investment)

- Promote the right Credit Card – You will find it in the Credit Card Section

- Earn incentives for each successful activation

Frequently Asked Questions – Increase Credit Limit

1. How long does it take to get a credit card limit increase in India?

If the increase is pre-approved, it can be instant after confirmation via SMS or app.

For manual requests, approval usually takes 3–7 working days, depending on document verification and bank policy.

2. Does requesting a credit card limit increase affect my CIBIL score?

If the bank performs a hard inquiry, your credit score may drop slightly (usually a few points). However, once your limit increases and your utilisation ratio decreases, your score may improve over time.

3. What credit score is required to increase a credit card limit?

Most banks prefer a CIBIL score above 750 for limit enhancements. Higher scores increase approval probability and may result in larger increases.

4. How often can I request a credit limit increase?

Most banks allow requests every 6–12 months, depending on your account performance and repayment history.

5. Is it better to increase my credit limit or apply for a new credit card?

It depends on your goal:

- Increase limit if you want better utilisation ratio and prefer managing one card.

- Apply for a new card if you want additional benefits like travel rewards or zero forex markup.

6. Will a higher credit limit make me eligible for premium credit cards?

A higher limit can improve your credit profile, but eligibility for premium cards also depends on income, employment category, and internal bank criteria.

7. Can self-employed individuals increase their credit card limit?

Yes. Self-employed users can request limit increases by submitting:

- ITR documents

- Business income proof

- Bank statements

Consistent repayment history is still the most important factor.

8. Does higher income automatically increase credit card limit?

No. Banks do not automatically update your income unless you submit proof. If your salary increases, inform the bank and provide supporting documents.

9. Can I temporarily increase my credit card limit for a large purchase?

Some banks offer temporary credit limit enhancements for specific transactions like travel bookings or high-value purchases. These are usually valid for a short period.

10. What is the ideal credit utilisation ratio?

Financial experts generally recommend keeping credit utilisation below 30% of your total limit to maintain a healthy credit score.

11. Why did my credit limit increase request get rejected?

Common reasons include:

- Recent late payments

- High credit utilisation

- Low credit score

- Unstable income

- Recent hard inquiries

Improving these factors before reapplying increases approval chances.

12. Does using my credit card frequently help increase the limit?

Yes. Active usage combined with consistent on-time repayment signals responsible behaviour and improves the likelihood of automatic upgrades.