The Slice vs SuperMoney credit card debate is one of the most relevant comparisons in India’s entry-level credit card space in 2026. Both are lifetime free RuPay cards. Both are UPI-enabled. Both are built for first-time credit card users. And both promise cashback on everyday spends without a rupee in fees. But they work very differently, and choosing the wrong one based on how you actually spend can mean earning half of what you could. This comparison breaks down both cards across every dimension that matters so you can make the call with numbers, not assumptions.

Slice vs SuperMoney Credit Card: Quick Comparison

Here is how both cards stack up before the detailed breakdown.

| Factor | Slice UPI Credit Card | Axis SuperMoney RuPay Card |

|---|---|---|

| Issuer | Slice Small Finance Bank x North East Small Finance Bank | Axis Bank x super.money by Flipkart |

| Network | RuPay, UPI-enabled | RuPay, UPI-enabled |

| Annual Fee | Nil, Lifetime Free | Nil, Lifetime Free |

| Base Cashback Rate | 2% on tap and scan transactions | 1% unlimited on all UPI and non-UPI spends |

| Accelerated Cashback | Up to 3% via Slice Spark weekly brand deals, not guaranteed every month | 3% on all UPI payments via super.money app |

| Cashback Cap | Not explicitly capped, varies by tier | No monthly cap, removed January 2026 |

| Cashback Type | Monies, redeemable within Slice ecosystem | Direct statement credit, no redemption needed |

| Forex Markup | Zero, no international transaction fee | Standard markup applies |

| Fuel Surcharge Waiver | 1% waiver up to Rs. 200 per cycle (transactions under Rs. 5,000) | 1% waiver on Rs. 400 to 4,000 transactions, max Rs. 400 per cycle |

| EMI Facility | Slice in 3, split purchases above Rs. 1,999 into 3 interest-free instalments | No equivalent feature |

| Lounge Access | None | None |

| Credit History Required | No, new-to-credit users eligible | No, entry-level card |

| CIBIL Reporting | Yes, reports as unsecured credit card post bank merger | Yes, Axis Bank reports to all credit bureaus |

| Card Replacement Fee | Rs. 300 + GST | As per Axis Bank schedule |

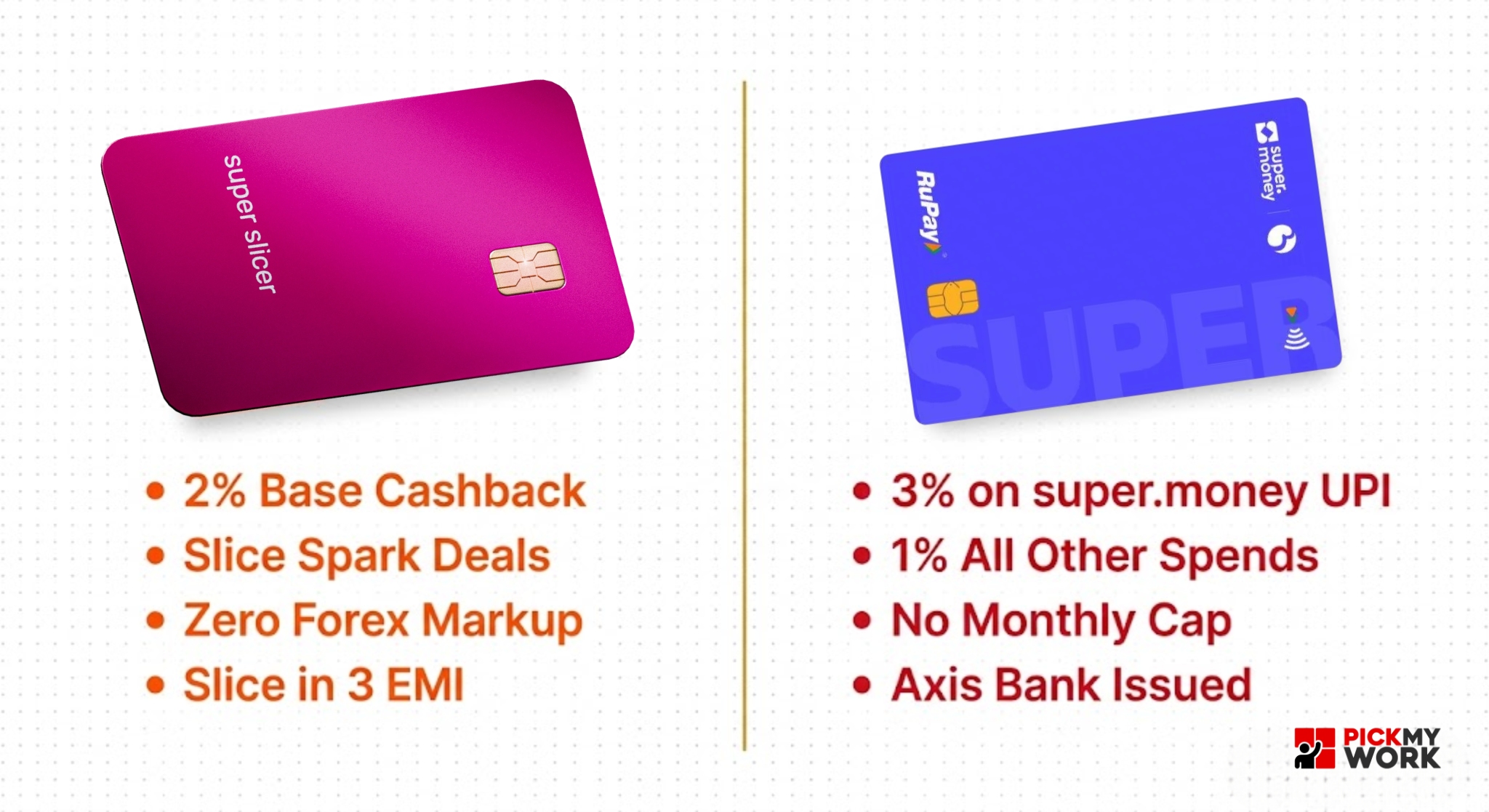

Slice Credit Card: How It Works and Who It Is For

The Slice UPI Credit Card is issued by Slice Small Finance Bank in partnership with North East Small Finance Bank, a fully RBI-licensed product that now reports as a proper unsecured credit card on your CIBIL report, following the completion of the bank merger in October 2024. The card works on the RuPay network and can be linked to Google Pay, PhonePe, and Paytm for UPI payments at any QR code merchant in India.

- Cashback structure: The base cashback is 2% on all tap and scan transactions. The advertised up to 3% requires activating a Slice Spark deal, a weekly rotating offer available in the app that applies enhanced cashback on a specific brand or category. Spark deals change every week and must be manually activated. If you do not activate a deal, you earn 2%.

- Cashback currency: Cashback on Slice is credited as Monies, which is Slice’s in-app currency. Monies can be used to pay your Slice bill, reducing your outstanding balance. They cannot be transferred to a bank account directly. This is a meaningful difference from direct cashback cards where savings appear automatically on your statement.

- Slice in 3: Any eligible purchase of Rs. 1,999 or more can be split into 3 equal interest-free instalments with no processing fee. This is a standout feature absent from most entry-level cards and useful for larger purchases like electronics, travel bookings, or clothing.

- Zero forex markup: Slice charges no foreign currency conversion fee, a rare and valuable feature at this fee tier. If you shop on international websites or travel abroad even occasionally, this alone makes Slice more cost-effective than most free cards.

- Best for: Someone who pays across multiple UPI apps, shops internationally online, wants the flexibility of 3-month interest-free EMIs on larger purchases, and is comfortable checking the Slice app weekly to activate Spark deals for maximum cashback.

Axis SuperMoney RuPay Card: How It Works and Who It Is For

The Axis Bank SuperMoney RuPay Credit Card is issued by Axis Bank in co-branding with super.money by Flipkart. It is Axis Bank’s strongest entry-level RuPay card and one of the highest-earning UPI cashback cards available in India in 2026, provided you make UPI payments through the super.money app specifically.

- 3% cashback on super.money UPI, with a key condition: The 3% accelerated cashback applies only to UPI transactions made through the super.money app. UPI payments made through Google Pay, PhonePe, or Paytm using this card earn only 1%, not 3%. This is a critical detail most comparison articles do not emphasise clearly enough. The card’s full value is realised only if super.money becomes your primary UPI app.

- A second condition on the 3%: The 3% cashback from super.money UPI payments cannot exceed the cashback earned from all other UPI and non-UPI spends in the same billing cycle. If your other spend cashback is below Rs. 100 in a month, the super.money cashback is capped at Rs. 100 regardless of how much you spend through the app. Spreading spending across both super.money and regular card transactions is what unlocks the full 3% consistently.

- No monthly cap as of January 2026: The earlier Rs. 500 monthly cashback cap was removed from January 1, 2026. This makes the card meaningfully more valuable for higher spenders who were previously capped regardless of spending volume.

- Direct statement credit: Cashback is credited directly to the card account 3 days before the next statement generation date with no activation, no app engagement, and no redemption process. It simply appears on your statement.

- Best for: Someone willing to use super.money as their primary UPI app, who makes a significant volume of UPI payments every month, and wants cashback to appear automatically without any weekly deal activation or loyalty programme management.

The Honest Cashback Reality: What You Actually Earn

Both cards advertise up to 3% cashback but the path to that 3% is completely different and the real-world effective rate for most users is lower than the headline. Here is what the numbers look like for a typical urban user spending Rs. 15,000 per month via UPI.

| Scenario | Slice Monthly Cashback | SuperMoney Monthly Cashback |

|---|---|---|

| Rs. 15,000 spend, no deal activation or all via super.money app | Rs. 300 (2% base, no Spark deal activated) | Rs. 450 (3% on super.money UPI) |

| Rs. 15,000 spend, Spark deal activated on primary category | Rs. 450 (3% on Spark category + 2% on rest) | Rs. 150 (1% base, if not using super.money app) |

| Rs. 15,000 spend, mixed across multiple UPI apps | Rs. 300 (2% flat, Slice works across all UPI apps) | Rs. 150 to 450 depending on how much goes via super.money |

The key takeaway: Slice earns more consistently across all UPI apps without any extra effort. SuperMoney earns more in absolute terms but only if you commit to using the super.money app as your primary payment method and meet the cashback condition on other spends. Neither card delivers its headline 3% automatically for every user in every month.

Slice vs SuperMoney: Pros and Cons

| Factor | Slice Wins | SuperMoney Wins |

|---|---|---|

| UPI App Flexibility | Works on any UPI app. GPay, PhonePe, Paytm all earn 2% | 3% only on super.money app, 1% elsewhere |

| Cashback Simplicity | Requires Spark deal activation for max value | Direct statement credit, fully automatic, zero effort |

| International Use | Zero forex markup, best on international online spends | Standard forex markup applies |

| EMI Flexibility | Slice in 3, interest-free 3-month split on Rs. 1,999+ purchases | No equivalent feature |

| Cashback Cap | No hard monthly cap | No monthly cap since January 2026, unlimited earning |

| Bank Credibility | Slice Small Finance Bank, newer institution | Axis Bank, India’s third largest private sector bank |

| Fuel Surcharge Cap | Rs. 200 per cycle | Rs. 400 per cycle, double the Slice cap |

Who Should Pick Which Card in 2026?

- Pick Slice if: You use multiple UPI apps and do not want to switch. You shop on international websites and want zero forex charges. You want the Slice in 3 EMI option for larger purchases. You are comfortable checking the app weekly to activate Spark deals for extra cashback.

- Pick SuperMoney if: You are willing to make super.money your primary UPI app for daily payments. You want cashback to appear automatically without any engagement effort. You trust Axis Bank as your card issuer. You spend heavily on UPI and want the uncapped 3% rate to compound over time.

- Pick both if: Both cards are lifetime free. There is no cost to holding both simultaneously. A practical strategy is to use the SuperMoney card for all UPI payments through the super.money app and the Slice card for international online purchases and larger EMI splits. Both build your CIBIL score in parallel.

Earn by Selling Entry Level UPI Credit Cards on PickMyWork

Entry-level credit cards are one of the most consistent earning categories on PickMyWork, and the reason is simple. Every student, young professional, homemaker, and first-time earner you know is a potential customer. The pitch does not require income proof, credit history, or complex eligibility conversations. Most open within 15 minutes on a phone. PickMyWork has active credit card tasks across multiple banks and fintech platforms. Open the app to see what is available in your city right now.

Related Reads

- Roarbank Credit Card Review 2026: 20% Cashback, Lifetime Free, UPI Explained

- Credit Card Against FD vs Regular Credit Card

- Credit Card Reward Points Explained: Earn, Redeem and Maximise Value

- Best UPI Credit Cards in India 2026

- Best Credit Cards for Rs. 50,000 Salary in India 2026

- All Credit Cards Available on PickMyWork

Frequently Asked Questions: Slice vs SuperMoney Credit Card

- Which is better, Slice or SuperMoney credit card in 2026?

It depends on how you pay. If you use multiple UPI apps and want consistent cashback without switching, Slice is better as it earns 2% across any UPI app. If you are willing to make super.money your primary UPI app, the Axis SuperMoney card earns 3% on those payments automatically with no monthly cap. Both are lifetime free so holding both simultaneously is a practical option at zero cost. - Does the Axis SuperMoney card give 3% cashback on all UPI apps?

No. The 3% accelerated cashback applies only to UPI payments made through the super.money app specifically. UPI payments made through Google Pay, PhonePe, Paytm, or any other UPI app using the SuperMoney card earn only 1% cashback. This is the most important detail to understand before applying for this card. - Is the Slice credit card really lifetime free?

Yes. The Slice UPI Credit Card has zero joining fee and zero annual fee, confirmed on the Slice Bank official website. There is a card replacement fee of Rs. 300 plus GST if your card is lost or damaged, but ongoing card ownership has no annual charges. - Does the Slice credit card build your CIBIL score?

Yes. Following the merger of SlicePay with North East Small Finance Bank completed in October 2024, the Slice card now reports as a proper unsecured credit card on your CIBIL report. Responsible usage, paying on time and keeping utilisation low, will positively impact your credit score over time. - What is the SuperMoney cashback cap in 2026?

The Axis Bank SuperMoney RuPay Credit Card removed its Rs. 500 monthly cashback cap from January 1, 2026. Cashback is now uncapped with no upper limit on how much you can earn per month. However, the 3% rate on super.money UPI cannot exceed the total cashback earned from all other non-super.money spends in the same billing cycle. - Can I use both Slice and SuperMoney credit cards together?

Yes, and this is actually a smart strategy. Both are lifetime free so holding both costs nothing. Use the SuperMoney card for all UPI payments through the super.money app to earn 3% cashback. Use the Slice card for international online shopping where its zero forex markup saves you money. Both cards build your CIBIL score simultaneously.

Also searched for: Slice vs SuperMoney which is better, Axis SuperMoney RuPay card review 2026, Slice UPI credit card review 2026, best lifetime free RuPay credit card India, UPI cashback credit card India 2026, Slice vs Roarbank, SuperMoney vs Kiwi credit card, best credit card for UPI payments India, new to credit card India 2026, best first credit card India 2026.